The tech sector losing streak has reached historic proportions as March 2026 draws to a close. With the technology sector on pace for its fifth consecutive monthly decline, investors are witnessing the longest run of monthly losses since September 2002 — a period that coincided with the dot-com bust aftermath. This alarming trend raises serious questions about the sustainability of the tech-driven rally that powered markets for much of the past three years.

Tech Sector Losing Streak: 5 Months of Relentless Selling

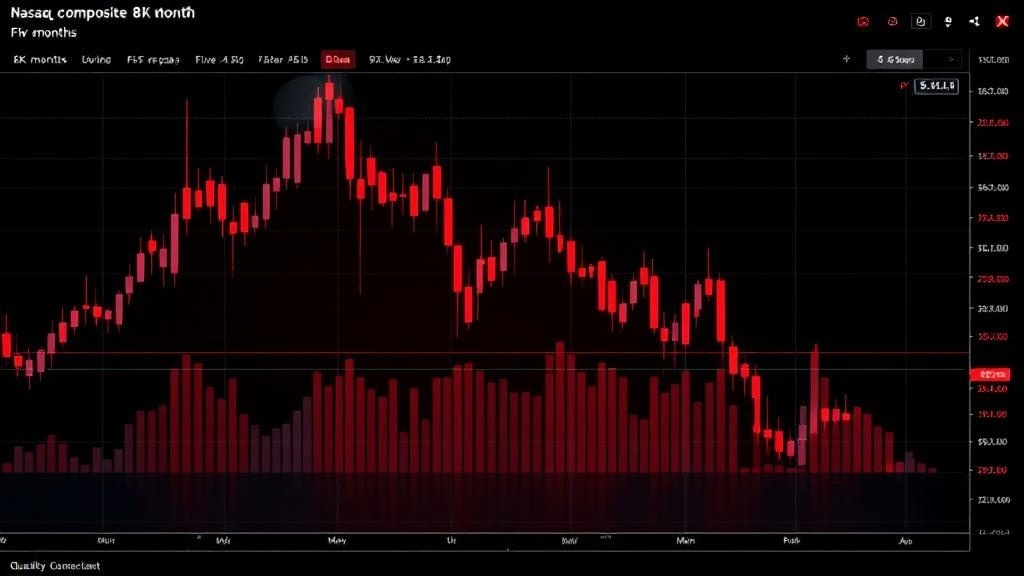

The numbers paint a grim picture for technology investors. The Nasdaq Composite entered this final week of March firmly in correction territory, down more than 10% from its recent highs. The S&P 500 isn’t far behind, having shed nearly 9% as the broader market follows tech lower. Five straight weeks of losses for major indexes have compounded the pain, with the Nasdaq 100 officially sinking into correction on March 27.

What makes this selloff particularly notable is its duration. Monthly losses stretching across November, December, January, February, and now March represent a systematic repricing of the sector rather than a temporary pullback. The last time technology stocks endured such a prolonged downturn, the industry was recovering from the excesses of the dot-com era.

What’s Driving the Extended Decline?

Several converging factors have created a perfect storm for tech stocks:

Oil Prices and Geopolitical Uncertainty

Crude oil surging above $100 per barrel has fundamentally altered the market landscape. The ongoing conflict involving Iran and concerns about the Strait of Hormuz have kept oil prices elevated, creating a headwind for growth-oriented sectors like technology. Higher energy costs eat into corporate margins and consumer spending power, both of which directly impact tech company revenues.

However, a glimmer of hope emerged when reports surfaced that President Trump told aides he’s willing to end the US military campaign even if the Strait of Hormuz remains largely closed. This development sent futures higher on Monday, though uncertainty about the conflict’s duration continues to weigh on sentiment.

AI Expectations vs. Reality

The artificial intelligence hype cycle has entered a critical phase. After massive capital expenditures by the “Magnificent Seven” tech giants, investors are increasingly questioning the return on investment timeline. Morgan Stanley recently lowered their price target on Meta to $775 from $825, though they still consider it a top pick, noting that “sentiment has troughed” due to GenAI ROIC and long-term positioning fears.

This tension between AI promise and near-term profitability has created a repricing mechanism across the sector. Companies that poured billions into AI infrastructure are now facing scrutiny over when — or whether — those investments will generate proportional returns.

Elevated Volatility and Risk Aversion

The Cboe Volatility Index (VIX) topped 31 last Friday and remains stubbornly above 30 — a level that historically signals significant market stress. Investors are paying premium prices for hedges, with a strong bias toward protective put options. This elevated fear gauge suggests that institutional money managers are bracing for further downside rather than positioning for a rebound.

How the Biggest Tech Names Are Faring

The damage has been widespread across big tech, though not evenly distributed:

Meta Platforms (META): Despite Morgan Stanley maintaining it as a top idea, the stock has faced persistent pressure from AI spending concerns and advertising market uncertainty. The social media giant exemplifies the broader tech dilemma — massive AI investment with uncertain near-term payoff.

Apple (AAPL): Supply chain concerns related to geopolitical tensions and a slowing consumer electronics refresh cycle have weighed on shares. The iPhone maker’s services revenue remains a bright spot, but hardware uncertainty dominates sentiment.

Nvidia (NVDA): The AI chip leader has seen significant volatility as investors debate whether the AI infrastructure buildout has peaked. Despite strong demand signals, the stock has been caught in the broader tech rotation.

Microsoft (MSFT): Cloud growth deceleration fears and heavy AI spending through its OpenAI partnership have pressured shares, though enterprise demand remains fundamentally solid.

Comparing This Selloff to 2002

The comparison to September 2002 is instructive but requires important context. In 2002, the tech sector was recovering from a genuine bubble burst — valuations had disconnected entirely from fundamentals, and many companies had no path to profitability. Today’s tech giants are massively profitable businesses with strong cash flows and dominant market positions.

However, the parallel isn’t entirely unfounded. Both periods share common themes: overinvestment in a transformative technology (the internet then, AI now), elevated valuations driven by future expectations, and external economic pressures that forced a repricing. The key difference is that today’s tech companies have real earnings power, which should provide a floor for valuations — albeit at lower levels than the euphoric peaks.

Small Caps Diverge from Large Cap Tech

An interesting divergence has emerged between large-cap tech and the broader market. While the Dow Jones Industrial Average rose 0.78% on Monday, the Russell 2000 small-cap index sat in the red, weighed down by biotech weakness. This pattern suggests that the market selloff is selective rather than indiscriminate — investors are repricing specific risk factors rather than dumping everything.

The S&P 500 earnings outlook remains a crucial variable. If corporate profits can outrun the oil shock and margin pressures, the current correction may prove to be a healthy repricing rather than the start of something more severe.

What History Says About Recovery Timelines

Historical data on extended tech selloffs offers both caution and hope. After the 2002 five-month losing streak ended, the Nasdaq took approximately 14 months to establish a durable bottom before beginning a sustained recovery. However, shorter multi-month declines — such as the 2018 Q4 selloff — reversed much more quickly once catalysts shifted.

Key factors that could trigger a reversal include:

- Resolution of geopolitical tensions: A ceasefire or oil price stabilization would remove a major headwind

- Positive AI earnings surprises: Concrete evidence that AI investments are generating returns

- Federal Reserve policy shift: Any dovish signals could reignite risk appetite

- Earnings season catalysts: Nike reports this week, and Q1 earnings season kicks off in mid-April

How Investors Should Position for Q2 2026

With the Q2 outlook uncertain, portfolio positioning becomes critical. Here are key considerations:

Don’t panic sell into weakness. Five months of selling has already repriced much of the risk. Investors who sold after similar historical declines often missed the subsequent recovery. The time to reduce tech exposure was at the highs, not after a correction.

Look for quality at a discount. Companies with strong balance sheets, consistent free cash flow, and dominant market positions — like Microsoft, Apple, and Alphabet — tend to recover fastest from corrections. Their fundamentals haven’t changed, even if their stock prices have.

Watch the VIX. A sustained move below 25 would signal improving sentiment and potentially mark an inflection point. Until then, expect continued choppiness and consider options strategies for downside protection.

Monitor oil prices closely. The tech sector’s recovery is partially hostage to geopolitical developments in the Middle East. A meaningful decline in crude would remove one of the key pressure points on equities.

The Bottom Line

The tech sector’s five-month losing streak is historically significant and shouldn’t be dismissed. The convergence of geopolitical risk, AI spending concerns, and elevated valuations has created a challenging environment that may persist into Q2. However, the underlying fundamentals of leading tech companies remain strong, and history suggests that such extended selloffs eventually create compelling entry points for long-term investors.

The key question isn’t whether tech will recover — it almost certainly will — but rather how much further the correction needs to run before sentiment stabilizes. With earnings season approaching and geopolitical developments evolving rapidly, April could prove to be a decisive month for the sector’s trajectory. Investors should stay informed, stay disciplined, and resist the urge to make emotional decisions in a volatile market.