Charter Communications closed a $1.3 billion pension termination buyout in January 2026, the first headline transaction of what insurers and consultants expect to be another record year for U.S. pension risk transfer. The Milliman 100 funded status sits at 103.8% with a $48.1 billion aggregate surplus, the strongest setup for plan sponsors looking to terminate or de-risk in over a decade. The question for finance committees is no longer whether to act, but how to document a fiduciary process that survives the next wave of post-deal litigation.

Key Takeaways

- Charter Communications closed a $1.3 billion pension plan termination via group annuity buyout in January 2026 (Pensions & Investments, Jan 30, 2026).

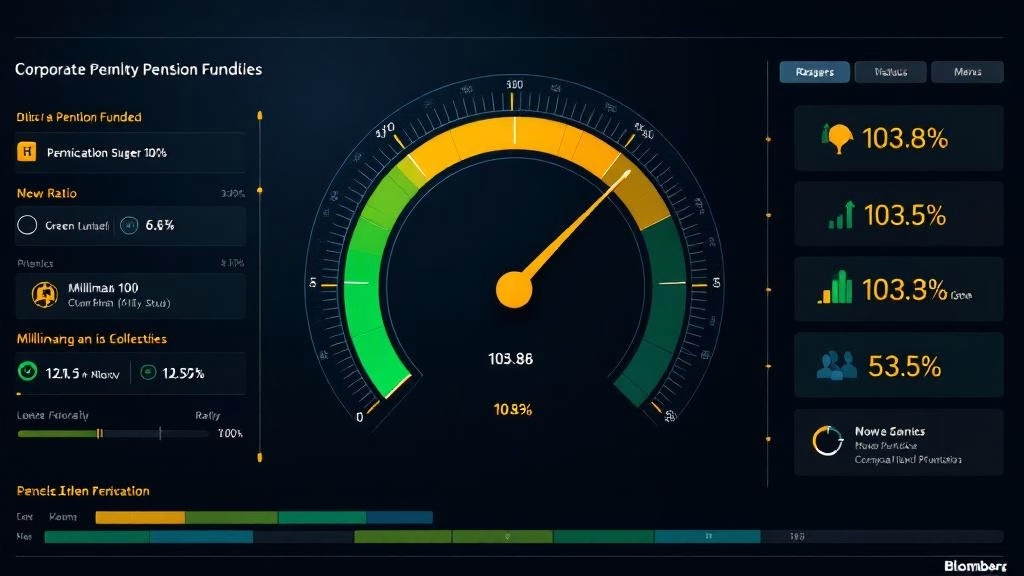

- The Milliman 100 corporate pension funded ratio reached 103.8% in fiscal 2025, up from 101.1% in 2024, with $48.1 billion in aggregate surplus across the largest U.S. corporate plans.

- J.P. Morgan Asset Management data shows 60% of the largest U.S. plans were overfunded in 2025, with combined surplus exceeding $85 billion.

- U.S. PRT buy-in volume reached $17 billion across 17 deals in 2025, a record, with insurers including Athene, MetLife, Prudential, Legal & General and Corebridge competing for mandates.

- The IBM lawsuit alleging $14 billion in PRT transfers to Prudential breached ERISA’s “safest available” standard remains the open litigation question that every CFO and pension committee must address before a 2026 termination.

What Is Driving the 2026 PRT Surge?

Three forces converge on the same calendar year. Funded status is at multi-decade highs. The Milliman 100 figure of 103.8% is the strongest reading since the firm began tracking the cohort, with 13 plans now exceeding 125% funded and none below 80%. The $20 Billion Club, which Russell Investments tracks separately, showed average funded ratios of 98.6% in 2025, with deficits compressed to $16 billion from $29 billion the prior year.

For the CFO, surplus changes the math. A plan funded at 110% has economic incentive to lock in the gain through a termination because the alternative is to keep the surplus on the balance sheet, where it generates no operating return and creates accounting volatility under ASC 715. A plan funded at 95% has the opposite calculus: terminate, and the sponsor must contribute the gap before the insurer takes over.

The second force is operating burden. Even an overfunded frozen plan still requires actuarial valuations, PBGC premiums, mortality experience studies, fiduciary investment oversight, and increasingly, the legal cost of defending past de-risking decisions. Charter’s calculus, like that of many telecom and cable peers, is that the operating cost of keeping a closed and frozen DB plan in run-off no longer pays for itself when the surplus is large enough to fund a clean exit.

The third force is interest rates. Higher long-end yields lower the present value of future pension liabilities and improve termination economics. The 2024-2025 yield environment held annuity buyout pricing competitive enough that BCG’s monthly pricing survey shows insurer all-in costs trending below the implied accounting liability for a meaningful portion of the year.

For the broader retirement context that frames sponsor decisions, our coverage of the SECURE 2.0 Section 101 auto-enrollment mandate explains why DB sponsors increasingly view the DC plan as the only retirement vehicle they want to operate going forward, and why DB termination accelerates that simplification.

Why Did Charter Pull the Trigger Now?

The Charter deal, reported by Pensions & Investments on January 30, 2026, transferred $1.3 billion of pension liabilities to a group annuity insurer. Plan terminations are not quick: actuarial work, PBGC notice, participant election windows for lump-sum offers, and final regulatory approval typically run 12 to 18 months from board authorization to closing date. That puts Charter’s authorization decision sometime in mid-to-late 2024, when funded status crossed the threshold most boards consider terminal-ready.

The standard rule of thumb consultants apply: a plan needs assets at roughly 102% to 110% of market liability to make termination economical. Below 102%, the sponsor must contribute cash to close the gap. Above 110%, the surplus exceeds what the insurer needs and the sponsor faces a reversion question. Charter’s $1.3 billion deal sits in the sweet spot where the math works without either large cash contribution or large surplus capture.

Telecom and cable sponsors have been the most active 2024-2026 PRT cohort because they share three traits: legacy DB plans frozen years ago, no recruiting need to maintain DB benefits for new hires, and stable cash generation that can absorb contribution top-ups if needed. Pitney Bowes disclosed approval of a 2026 plan termination in its 2025 10-K, and the Pensions & Investments PRT calendar continues to load.

Who Are the Insurers Competing for the Mandates?

Three insurers historically dominate U.S. PRT volume:

- Athene, the Apollo-affiliated annuity provider, has been the most aggressive 2024-2026 bidder.

- MetLife, with the longest track record in U.S. group annuity transfer, retains the relationship advantage with the largest sponsors.

- Prudential, named lead insurer on the September 2024 IBM $6 billion transfer and one of the two providers on the September 2022 IBM $16 billion split with MetLife.

Together those three captured roughly two-thirds of 2022 PRT volume by ResearchAndMarkets data. The next tier – Legal & General Retirement America, Corebridge Financial, Pacific Life, Mass Mutual, Principal, and Western & Southern – competes aggressively on smaller and mid-size mandates and increasingly takes lead positions on $500 million to $2 billion deals.

The 2025 calendar produced $17 billion in U.S. buy-in volume across 17 deals, a record, according to data tracked by Aon’s PRT practice. Buyouts (where the sponsor terminates the plan and transfers all obligation to the insurer) and buy-ins (where the sponsor purchases an annuity contract held as a plan asset, with no immediate termination) are the two main structures. The buy-in volume record matters because it signals that even sponsors not ready for full termination are using the strong-funded environment to lock in liability matching.

For comparison with the broader institutional flow story, our analysis of the 7 trillion money market cash wall covers the parallel conservative-asset migration on the household and corporate side.

How Are PRT Lawsuits Changing Sponsor Selection Criteria?

The legal overhang that nearly stalled 2024 PRT activity has not disappeared. The IBM litigation, filed in U.S. District Court for Massachusetts, alleges that IBM and its independent fiduciary State Street Global Advisors violated ERISA when they selected Prudential as the annuity provider for $14 billion of pension transfers across 2022 and 2024. The plaintiffs argue Prudential is not the “safest available” annuity provider as ERISA Interpretive Bulletin 95-1 requires.

A separate Lockheed Martin/Athene case, now in motion practice, raises similar questions about transfers to private-equity-affiliated annuity providers. The fiduciary playbook that has emerged across 2025 to 2026 sponsor counsel includes:

- Independent fiduciary engagement with documented selection criteria beyond price.

- Multi-insurer bid competitions with at least three carriers, even when one is the obvious lead.

- Documented analysis of insurer capital adequacy, asset quality, reinsurance exposure and PE affiliation.

- Participant communications addressing the difference between insurer-backed annuity protection and PBGC pension protection.

Pensions & Investments reporting suggests the 2026 outlook is “strong as lawsuit fears diminish,” driven by early court rulings that have generally credited well-documented fiduciary processes. That shifts the issue from whether to do PRT to how to defend the decision.

For the broader retirement reform context, our coverage of the SECURE 3.0 OPTIONS Act 2026 roadmap explains the legislative backdrop that has generally been favorable to plan sponsor de-risking.

What Should Plan Sponsors and Consultants Watch Through Q3 2026?

Five data points to track through mid-year:

- Quarterly Milliman 100 and Mercer S&P 1500 funded status updates. A retreat below 100% would slow termination calendars; sustained 102%+ would accelerate them.

- BCG monthly annuity pricing survey trend. PBGC now licenses this data, which signals it has become the de facto market reference for fiduciary documentation.

- The Charter deal carrier disclosure. When Charter files its 10-K and audited annuity contract details become public, the carrier identity will set comparable pricing benchmarks for the next wave.

- District court rulings in IBM and Lockheed cases. A defense win solidifies the fiduciary playbook; a plaintiff win would reset deal timelines.

- PE-affiliated insurer capital adequacy disclosures. Athene, F&G, Global Atlantic and similar entities are the swing-vote capacity providers in the PRT market.

For sponsors comparing PRT to alternative DB exit paths, our coverage of alternative investments inside 401(k) plans under the April 2026 DOL rule covers the parallel question of how the DC side absorbs the asset migration.

Three Questions for the Plan Sponsor Pension Committee

Before the next quarterly meeting, the CFO, the head of HR and the independent fiduciary should be able to answer:

- Have we modeled termination economics at current 103-108% funding levels versus the 5-year holding cost of operating the plan in run-off? The hold-cost calculation needs to include PBGC premiums, actuarial fees, fiduciary investment management, audit cost, and the present value of expected mortality experience.

- Is our independent fiduciary process documented to the standard the IBM and Lockheed dockets are establishing? A bid log with at least three carriers, documented selection criteria, and capital adequacy analysis is the new floor.

- What is our communication plan for participants regarding the shift from PBGC pension guarantee to state-guaranty-association annuity protection? Participants increasingly receive class-action solicitation letters within weeks of any PRT announcement.

The Charter $1.3 billion termination is the opening shot of 2026, but the deal pipeline that consultants and insurers describe in private is materially larger than 2024-2025 combined. With funded status at multi-decade highs and the legal playbook clarifying, the question for every plan sponsor with a frozen DB plan is no longer whether the math works. It is whether the process documentation will hold up in court three years after closing.

Figures and dates as of May 2026. Sources: Pensions & Investments PRT coverage (Jan 30, 2026); Milliman 100 Pension Funding Study (fiscal 2025); J.P. Morgan Asset Management corporate pension surplus analysis; Russell Investments $20 Billion Club report; ResearchAndMarkets U.S. PRT Market Insights 2025-2030; PLANADVISER and PLANSPONSOR IBM litigation coverage; Aon PRT practice annual review; BCG Pension monthly annuity buyout pricing survey.

About Me

Founder and Chief Research Analyst at Trading Market Signals. Abdelali El Khadmaoui specializes in AI Wealth Intelligence, Wealth Management, Registered Investment Advisors (RIAs), Family Offices, Retirement Planning and Private Credit. He publishes in-depth research and data-driven analysis for financial professionals.

Just as They Gate Redemptions: The Liquidity Factor Sponsors Must Document")

: The In-Plan Lifetime Income Push of 2026")